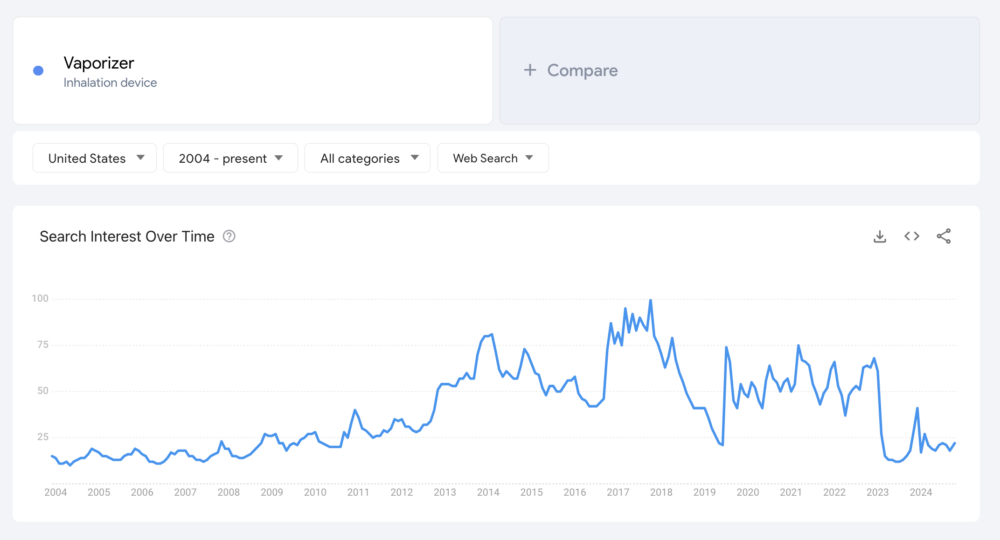

The nicotine industry has changed a lot over the years. Fewer people smoke cigarettes now because of health warnings, strict laws, and higher taxes. But companies still need to make money. To do that, they’ve started selling new kinds of nicotine products called Next Generation Products (NGPs). These include:

- E-cigarettes (ENDS): Devices that let people inhale nicotine vapor instead of smoke.

- Heated Tobacco Products (HTPs): Devices that heat tobacco to create vapor but don’t burn it.

- Nicotine Pouches: Tobacco-free products you put in your mouth to absorb nicotine.

- Snus: Moist tobacco placed under the lip, popular in Scandinavia.

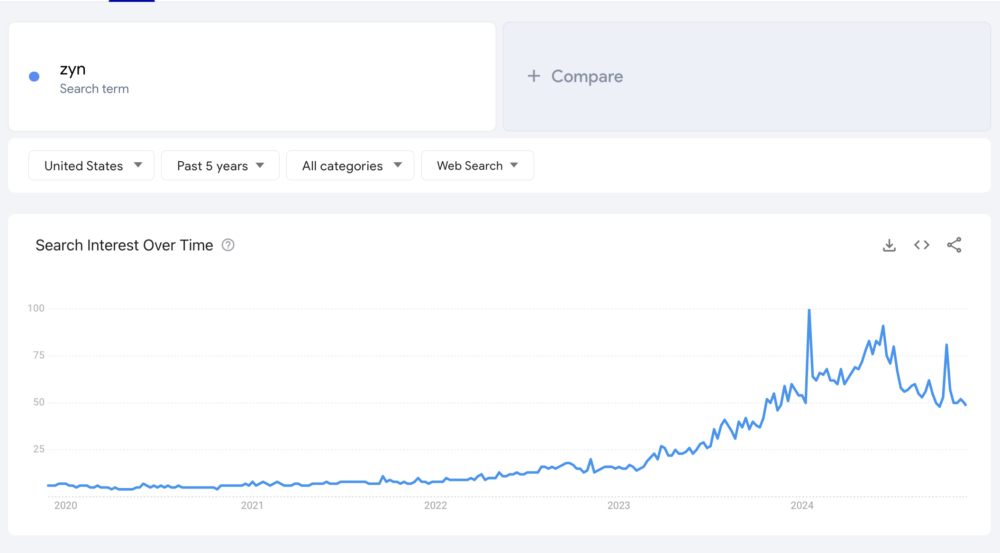

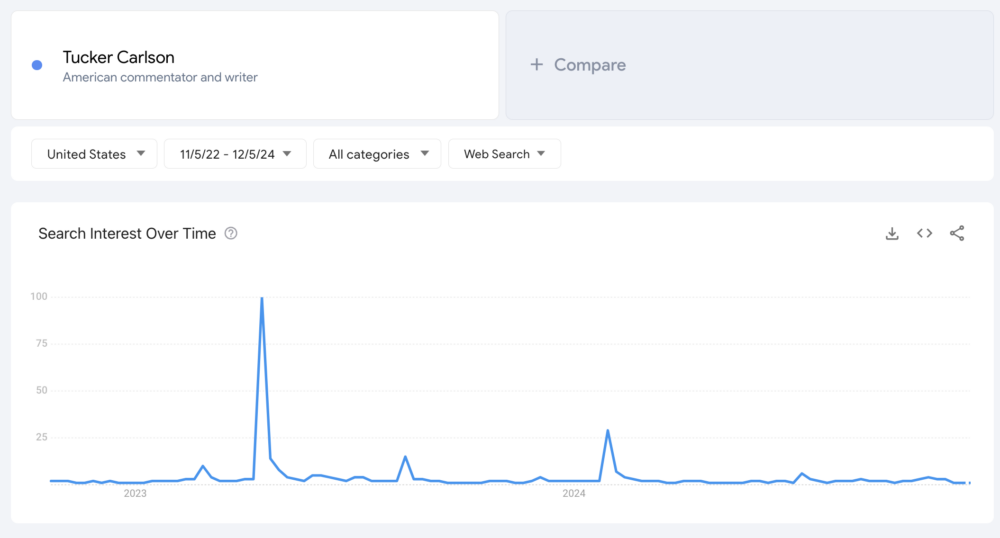

One big category today is nicotine pouches. Zyn, the market leader, has been around for a while. But now a new brand called ALP, created by Tucker Carlson, wants to shake things up. ALP markets its product as stronger and cheaper, creating a challenge for Zyn. This rivalry raises questions: is Zyn vs. Alp the next nicotine war? Or will we see the next wave of innovation instead?

A Decade of Disruption: The Sequence of Nicotine Innovation

The past ten years have brought many changes in how people use nicotine. Each new phase has introduced different products and ideas, shaping the market and how people view harm reduction.

Phase 1: Traditional Vapes (mid 2000s–2015)

The first modern e-cigarettes, like Blu and NJOY, became popular during this time. These devices allowed people to inhale vapor instead of smoke, avoiding many harmful chemicals found in cigarettes. They used refillable tanks that people could customize with different flavors and nicotine levels.

Smokers liked that these vapes gave them a similar experience to smoking. They could hold the device, take a puff, and see the vapor. But these products had problems too. They were bulky, required frequent cleaning, and were hard to use for some people. While they helped many smokers quit, they didn’t catch on with everyone.

There were doubts about the health benefits behind traditional vapes and a number of studies showed that they cause permanent lung damage. Prices were expensive and ultimately pod systems like Vuse took over the market for casual e-cigarette users.

Phase 2: Vuse and Pod Systems (2015–2017)

Pod systems like Vuse made vaping easier and more convenient. Instead of messy refillable tanks, these products used pre-filled pods. Users didn’t have to worry about spills or maintenance. This simplicity attracted more smokers who found traditional vapes too complicated.

Pod systems were also smaller and easier to carry around. They became popular among smokers who wanted to quit without a steep learning curve. Companies also marketed them as sleek and modern. However, these products didn’t completely solve the problem of getting more smokers to switch, as many still preferred traditional cigarettes and found the flavors of Vuse less desirable.

importantly, Vuse is still in the mix of major players due to their strategic marketing and branding efforts, which have ensured relatively linear growth over the last 7 years, although with a decline since 2022.

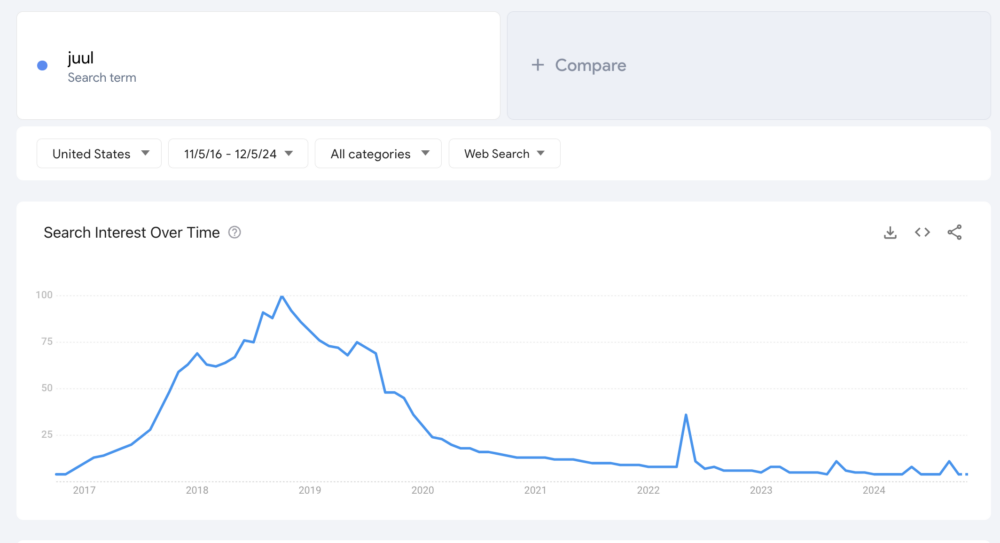

Phase 3: Juul Dominance (2017–2019)

Juul changed introduced nicotine salt technology, which made the nicotine hit feel more similar to a cigarette than traditional pod systems. Smokers who tried Juul said it felt more satisfying than older vapes. Juul also became a cultural phenomenon, thanks to social media and their marketing approach, which ultimately ended up being the same cause of their fall a few years later.

By 2018, Juul controlled 76% of the U.S. e-cigarette market. But its success came with problems. Critics proved Juul’s fruity flavors and flashy ads targeted teenagers too much. This led to a vaping epidemic among young people. Regulators cracked down, and Juul took a major hit.

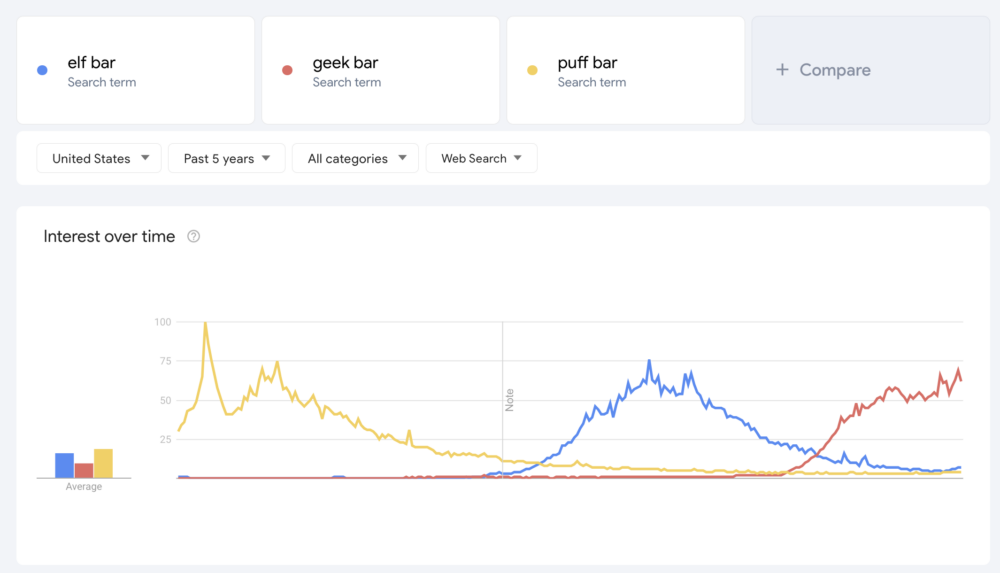

Phase 4: Disposable Vapes (2020–2024)

When Juul faced stricter rules, disposable vapes like Geek Bar, Elf Bar, and Puff Bar filled the gap. These products are cheap, easy to use, and pre-filled with liquid. Users don’t need to recharge or replace parts—just throw it away when it’s empty.

Disposables became a hit with younger users, taking a page from the Juul marketing book. But just like Juul, regulators are noticing that these products are most not earning money by getting people to switch away from traditional cigarettes, but instead, are recruiting new smokers–and mostly younger ones.

Nationwide bans are in discussion in countries like the United Kingdom. The FDA has warned hundreds of retailers to stop selling the products because they target children and teenagers. While they are still around, their popularity is much lower.

Puff bar was the first to trend between February and October 2020. Amid the trending surge, the FDA banned it for targeting children and teenagers with its fruity flavors like OMG (Orange, Mango, Guava). A couple years later, Chinese brand Elf Bar entered the mix, trended highly as well. The FDA has focused on penalizing retailers who sell Elf Bar due to difficulty regulating the foreign brand’s imports. Now, we are seeing the peak of Geek bar, which has a nearly identical rise in consumer search behavior as Elf Bar, the ongoing new trend of disposable vapes. We can presume where that is likely to go as history tends to repeat itself.

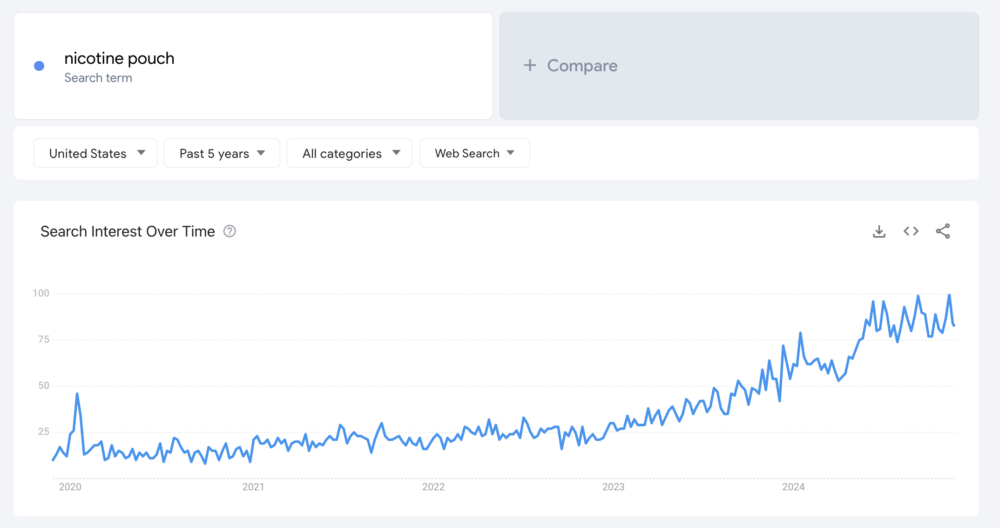

Phase 5: Nicotine Pouches (2023–Present)

Nicotine pouches like Zyn became popular because they’re smokeless and spit-free. Users place the pouch under their lip, where it releases nicotine over time. These products are discreet and don’t produce smoke or vapor, making them ideal for harm reduction.

Zyn is the leader in this category, offering nicotine options from 3mg to 6mg. Zyn claims smokers use it as a stepping stone to quit altogether. However, there are challenges. Some people think pouches are just as harmful as cigarettes. Reported the biggest hit since cigarettes by CNN, Zyn also targets young people and is criticized for its marketing strategy efficacy.

Now, ALP is entering the market with a celebrity marketing approach, endorsed by Tucker Carlson, a Russian propagandist who notoriously called Ukrainian President Zelenskyy a dictator while getting close to and praising authoritarian Vladimir Vladimirovich Putin. ALP wants to compete directly with Zyn.

If Carlson successfully rides the MAGA wave, ALP could become the next brand in the spotlight. But early indications are not yet optimistic. Carlson’s cultural relevance remains smaller than we thought and consumers have remained relatively quiet amidst the launch. We believe it may be due to a lack of brand differentiation and over-estimation of Carlson’s impact on sales.

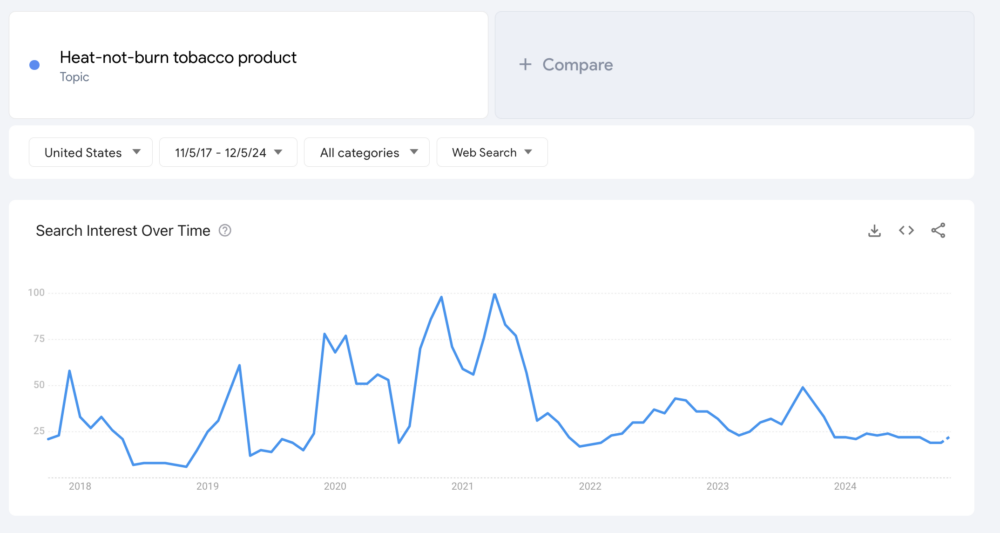

Phase 6: Heated Tobacco Products (HTPs)

Heat-not-Burn tobacco products are devices like IQOS, Glo, and Ploom X. They heat tobacco to create vapor without burning it. Companies claim this reduces harmful toxins compared to traditional smoking. HTPs have been very successful in Japan and South Korea, where e-cigarettes are less common.

However, HTPs haven’t caught on everywhere. In the U.S. and Europe, they’re still niche products due to strict regulations and patent disputes. Some health experts also question how much safer HTPs really are. Despite these challenges, companies continue to push HTPs as the next big thing in harm reduction.

Potential Trend Ideas

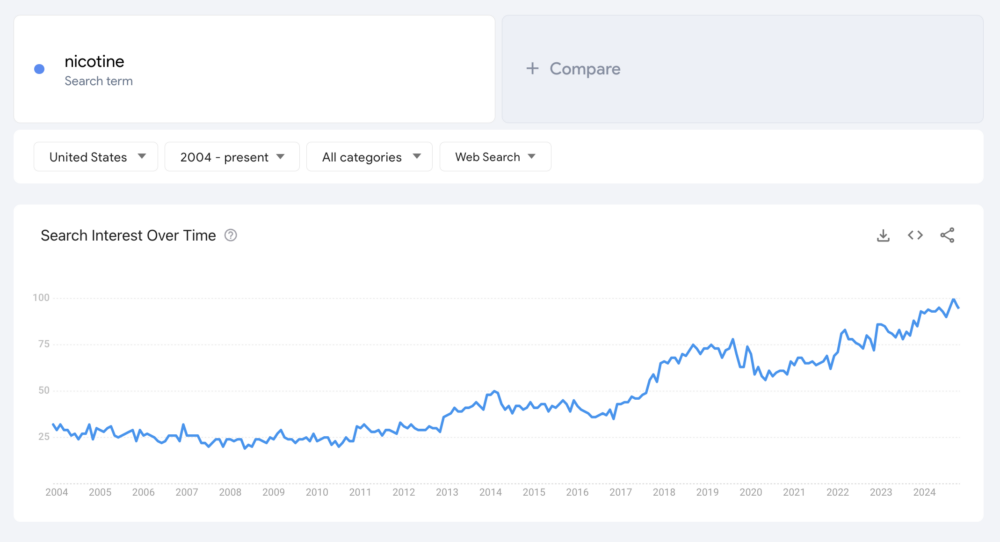

Despite only 11 percent of Americans smoking cigarettes, demand for nicotine is actually growing at a rapid rate and only expected to continue growing.

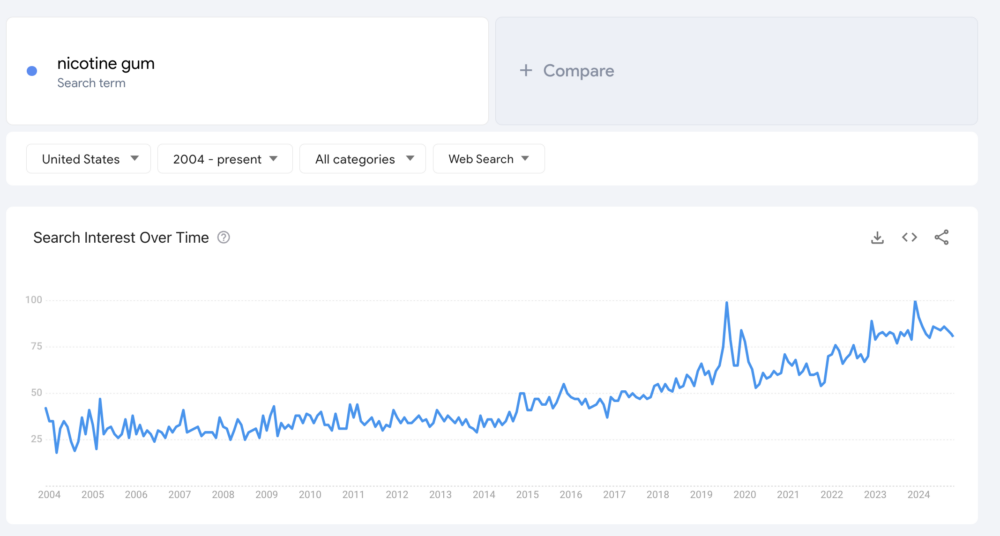

Nicotine gum remains extremely popular, too, mirroring the overall growth trend around nicotine.

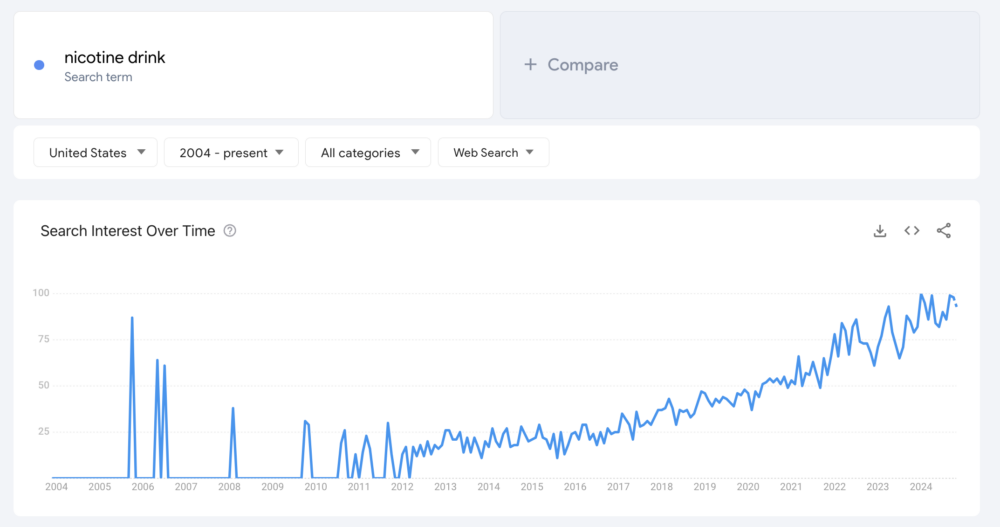

One thing we think could be the next area we see innovation around could be nicotine drinks. Nicotine drinks are beverages infused with small amounts of nicotine. The goal is to deliver a mild stimulant effect similar to coffee or energy drinks. They are an emerging concept aimed at offering a discrete, convenient, and alternative way to consume nicotine. These drinks could be carbonated, flavored, or alcoholic (the nicotini).

They are not yet mainstream but growing very quickly lately.

Conclusion: Zyn Wins but Nicotine Pouches May Be a Passing Trend

Zyn is likely to hold its spot as the leader in nicotine pouches. With the backing of Swedish Match, Zyn has the resources and reputation to stay ahead of newer brands like ALP. ALP’s lack of unique features and over-reliance on celebrity marketing make it hard to compete in a market that rewards trust and consistency.

Still, nicotine pouches might not stay popular forever. Just like other nicotine products—such as pod systems and disposable vapes—trends in this industry can fade quickly. The next big thing, like nicotine drinks, could shift consumer focus away from pouches in just a few years.

Zyn may beat ALP, but the real test will be whether it can adapt when the market inevitably changes again.